This website uses cookies to facilitate navigation, registration and collection of statistics. The information stored in cookies is used exclusively by our website. When browsing with active cookies consents to its use.

Historically a strong global Defense market, the UK is also focusing on the Space sector, mainly due to low aircraft assembly capabilities

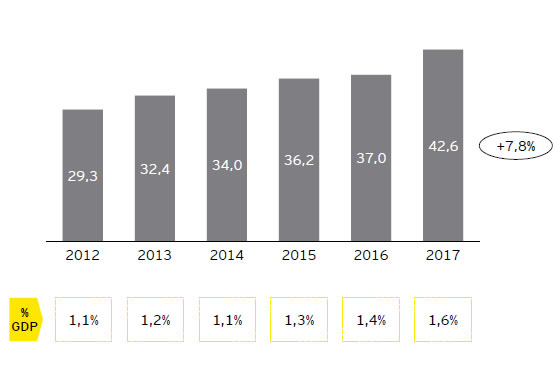

UK ASD industry overview

2012-17 CAGR

2012-17 CAGR

| The British ASD industry grew by 7,8%/ year, reflecting an increase of 0,5 pp in % GDP (2012-17) |

UK ASD revenues[€bn, 2012-17]

- In 2012-17, the UK government increased its ESA(1)contribution to reach 25% in public spending, attracting FDI2from major players

- UK Space sector represents 10% of the global Space turnover, and is one of the largest suppliers of global nanosatellites currently in orbit

| Small satellites manufacturing and cybersecurity are the main drivers for continuing growth |

Aeronautics

- To meet global environmental targets, government is investing €106 million in the next years to develop new aircraft generations (e.g., electric aircraft solutions)

- To improve manufacturing productivity, efficiency and spending in R&D, government invested €103 million in 2018

Space

- Government ambitions for the sector include the growth of Space tourism, planning on investing €20 billion in the next 20 years

- The UK’s Space sector has manufactured 40% of the total small satellites in orbit and forecasts a 10% capture of the global Space sector by 2030

Defense

- Pressure to reach the NATO’s 2,0% of GDP and a forecast of more than €7 million security exports in 2022 (+30% than 2018) led to the increase of the 2017 Defense budget by 1,4% (reaching €42,6bn)

- Due to more than €5,5million year of cyber offences in the UK (half of the total national crime), the government is investing €25 million in Defense R&D

Notes: (1) ESA -European Space Agency; 2) FDI –Foreign Direct Investment

Sources: ADS, MarketLine, UK Government, Mergent, Business Matters, World Finance, EY analysis